Healthcare Analytics Market Size ,Share Report , 2033

Global Healthcare Analytics Market Size

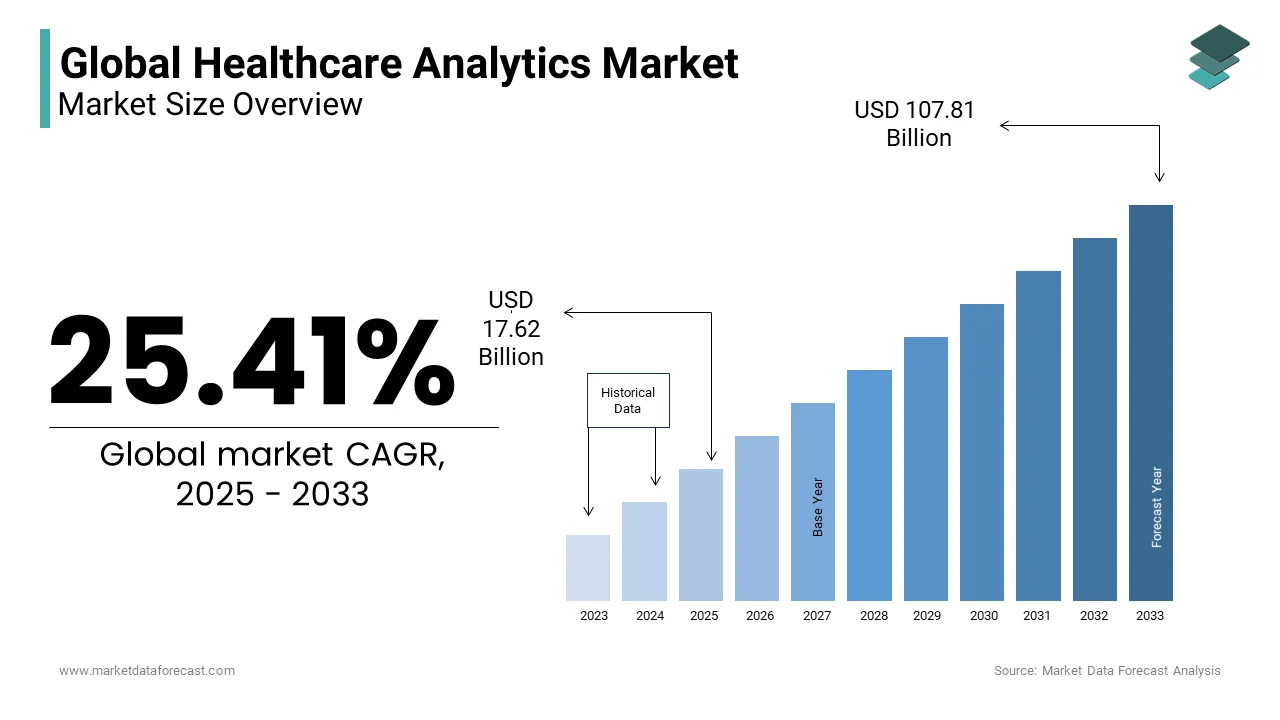

The global healthcare analytics market size was valued at USD 14.05 billion in 2024. The healthcare analytics market size is expected to have a 25.41% CAGR from 2025 to 2033 and be worth USD 107.81 billion by 2033 from USD 17.62 billion in 2025.

Healthcare Analytics is the application of advanced data analysis techniques to transform vast volumes of clinical, operational, financial, and patient-generated health data into actionable insights. It leverages technologies such as artificial intelligence, machine learning, natural language processing, and predictive modeling to enhance clinical decision-making, improve patient outcomes, and streamline healthcare delivery. As healthcare systems globally transition from fee-for-service to value-based care models, analytics has become instrumental in monitoring quality metrics, reducing care variability, and managing population health. The integration of electronic health records (EHRs), wearable devices, and real-time monitoring systems has exponentially expanded the data ecosystem.

Additionally, the proliferation of telemedicine, accelerated by the pandemic, has further amplified the need for real-time analytics to manage remote patient monitoring and virtual care coordination.

MARKET DRIVERS

Rising Burden of Chronic Diseases Driving Demand for Predictive Analytics

The escalating global prevalence of chronic diseases is a pivotal driver accelerating the adoption of healthcare analytics, particularly predictive and prescriptive models. Cardiovascular diseases, diabetes, and cancer collectively account for over 70% of global deaths annually, as reported by the World Health Organization. In the United States alone, the Centers for Disease Control and Prevention indicate that 60% of adults suffer from at least one chronic condition, responsible for 90% of the nation’s $4.1 trillion annual healthcare expenditure. This immense clinical and economic burden necessitates early intervention and risk stratification, capabilities inherently enabled by advanced analytics. Furthermore, the ability to analyze longitudinal patient data, genetic profiles, and lifestyle factors allows providers to shift from reactive to proactive care. In population health management, analytics facilitates targeted interventions for at-risk cohorts, improving outcomes while reducing system strain. As chronic disease rates continue to climb, the demand for scalable, data-driven solutions becomes indispensable, positioning healthcare analytics as a core component of sustainable care delivery.

Expansion of Electronic Health Records and Interoperability Initiatives

The widespread adoption and maturation of electronic health records (EHRs) have laid the foundational infrastructure for the proliferation of healthcare analytics. Beyond mere digitization, the emphasis has shifted toward interoperability enabling seamless data exchange across disparate systems. The 21st Century Cures Act, enacted in 2016, mandated standardized APIs, catalyzing the development of analytics platforms capable of aggregating data from multiple sources. This cross-border data integration enhances the robustness of analytics models by expanding sample sizes and diversity. Moreover, the technical advancement allows real-time data access, crucial for dynamic analytics in clinical decision support. With EHRs generating over 150,000 data points per patient annually, as estimated by Johns Hopkins Medicine, the capacity to derive insights from this volume is only achievable through advanced analytics. Consequently, the evolution of EHR ecosystems from static repositories to intelligent data engines is fundamentally reshaping the analytical landscape in healthcare.

MARKET RESTRAINTS

Data Privacy Concerns and Regulatory Fragmentation Impeding Market Growth

Despite the transformative potential of healthcare analytics, persistent concerns surrounding data privacy and security significantly restrain market expansion. Sensitive health information is a prime target for cyberattacks, with healthcare experiencing more breaches than any other sector. According to the U.S. Department of Health and Human Services, over 133 million patient records were exposed in 725 reported breaches in 2023 alone. The average cost of a healthcare data breach reached $10.93 million per incident in 2023, the highest across all industries, as detailed by IBM’s Cost of a Data Breach Report. These vulnerabilities erode patient trust and deter data sharing, essential for robust analytics. Regulatory frameworks further complicate the landscape. While the European Union enforces the stringent General Data Protection Regulation (GDPR), the United States operates under a patchwork of state and federal laws, including HIPAA, which lacks uniformity in enforcement and scope. As per the Commonwealth Fund, only a limited number of healthcare organizations report full compliance with cross-jurisdictional data governance standards. In emerging markets, weak legal infrastructure exacerbates risks. Additionally, patient consent mechanisms remain inconsistent. These factors collectively inhibit the aggregation of large, diverse datasets required for advanced analytics, particularly in AI training. Until harmonized, enforceable privacy standards are established globally, the full potential of healthcare analytics will remain constrained by legitimate security and ethical concerns.

Shortage of Skilled Data Professionals in the Healthcare Sector

The acute shortage of professionals equipped with both clinical knowledge and advanced data science expertise is a critical structural restraint on the healthcare analytics market. The integration of analytics into care delivery demands a hybrid skill set understanding medical terminology, regulatory environments, and statistical modeling which remains rare in the current workforce.

As per the U.S. Bureau of Labor Statistics, demand for medical and health services managers with data analytics proficiency is projected to grow from 2021 to 2031, far outpacing supply. Academic institutions are not producing graduates at a sufficient rate. This talent gap delays analytics implementation. Moreover, existing clinicians often lack training in data interpretation; only a limited number of physicians feel confident using predictive analytics in clinical decisions. In low-resource settings, the deficit is more severe, with data specialists conspicuously absent from workforce planning. Without targeted investment in interdisciplinary education and upskilling, the scalability of healthcare analytics will remain fundamentally limited by human capital constraints.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Clinical Decision Support Systems

The convergence of artificial intelligence (AI) with clinical workflows presents a transformative opportunity for the healthcare analytics market, particularly in diagnostic accuracy and treatment personalization. AI-powered analytics tools are increasingly embedded in radiology, pathology, and genomics to augment physician decision-making.

For example, deep learning algorithms in mammography interpretation have demonstrated a reduction in false negatives compared to human radiologists. The Mayo Clinic has implemented an AI-driven ECG analysis that detects asymptomatic left ventricular dysfunction with high accuracy, enabling early intervention. Furthermore, in oncology, platforms like IBM Watson for Clinical Trial Matching use natural language processing to analyze unstructured physician notes and match patients to trials, reducing screening time. As computational power grows and algorithmic transparency improves, AI-driven analytics will transition from adjunct tools to integral components of precision medicine, fundamentally redefining diagnostic paradigms and therapeutic planning across specialties.

Growth of Remote Patient Monitoring and Wearable Technology Ecosystems

The rapid proliferation of remote patient monitoring (RPM) and wearable health technologies is generating unprecedented volumes of real-time physiological data, creating fertile ground for advanced healthcare analytics. Devices such as continuous glucose monitors, smartwatches with ECG capabilities, and implantable cardiac sensors produce continuous data streams, enabling longitudinal health tracking. The Veterans Health Administration pointed out a reduction in hospital admissions among patients using RPM for chronic conditions, demonstrating tangible clinical impact. Apple’s Heart Study, involving over 400,000 participants, revealed that algorithm-driven notifications led to the timely diagnosis of atrial fibrillation in 0.5% of users, as per The New England Journal of Medicine. Similarly, Fitbit’s partnership with Google Health has enabled large-scale analysis of activity and sleep patterns to predict early signs of metabolic syndrome. As per the American Telemedicine Association, RPM adoption increased significantly between 2020 and 2023, driven by CMS reimbursement expansions. The integration of these devices into electronic health systems allows predictive modeling of exacerbations in conditions like heart failure and COPD, transforming episodic care into continuous, data-informed management.

MARKET CHALLENGES

Ensuring Data Quality and Standardization Across Heterogeneous Sources

The inconsistency and poor quality of data sourced from disparate systems are one of the most persistent challenges in healthcare analytics. Despite digitalization, healthcare data remains fragmented across EHRs, claims databases, lab systems, and patient-generated inputs, often in non-standardized formats. In the US, many of the EHR data entries contain inaccuracies, including missing values, duplicate records, and incorrect coding. The lack of uniform terminology exacerbates the issue only half of U.S. hospitals use standardized clinical vocabularies like SNOMED CT, as per the Office of the National Coordinator for Health IT. This heterogeneity undermines the reliability of analytics models, particularly machine learning algorithms that depend on clean, structured inputs. For instance, an investigation in JAMA Internal Medicine revealed that predictive models for sepsis failed in many of the external validations due to data drift and inconsistencies in vital sign documentation. In low-resource settings, paper-based records still constitute a notable portion of patient documentation. Even in advanced systems, unstructured data such as physician notes accounts for a significant share of clinical information, requiring complex natural language processing to extract meaning. The absence of global data governance frameworks compounds the challenge. Without rigorous data curation, normalization, and validation protocols, even the most sophisticated analytics platforms risk generating misleading insights, ultimately compromising patient safety and decision integrity.

Balancing Algorithmic Transparency with Clinical Trust and Adoption

The opacity of advanced analytics models, particularly those based on deep learning, poses a significant challenge to their acceptance by clinicians and patients. Known as the “black box” problem, the inability to interpret how algorithms arrive at specific conclusions undermines trust in their recommendations. Many physicians hesitate to follow AI-generated diagnostic suggestions due to a lack of explainability. In critical care settings, where decisions carry life-or-death consequences, this skepticism is amplified. For example, an AI model predicting ICU mortality developed by Stanford University achieved high accuracy but was rejected by clinicians because it relied on non-intuitive variables, such as admission time and bed location, as per a 2022 case study published in NPJ Digital Medicine. Regulatory bodies are responding the FDA now requires manufacturers to submit algorithm transparency documentation for AI-based SaMD (Software as a Medical Device). However, a limited portion of commercially deployed models provides clinically interpretable outputs. In radiology, despite AI’s ability to detect lung nodules, radiologists report discomfort when the system cannot justify its findings visually. The European Commission’s 2024 AI Act mandates “human-in-the-loop” oversight, emphasizing the need for interpretable models. Until analytics platforms can deliver not only accuracy but also clinical intelligibility, their integration into routine practice will remain partial, limiting their transformative potential across healthcare ecosystems.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

Based on Component, Application, Deployment Mode, End User, Delivery Mode, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

|

Market Leaders Profiled |

SAS Institute Inc., McKesson, Optum Inc., IBM Corporation, Truven Health Analytics Inc., Cerner Corporation, Verisk Analytics Inc., Allscripts Health Solutions, Oracle CorporatiMedeAnalyticsAtics, Inovalon Inc., and Health Catalyst. |

SEGMENTAL ANALYSIS

By Component Insights

The software segment commanded the healthcare analytics market by accounting for a 62.4% share in 2024. This dominance of the segment is due to the foundational role of analytics platforms in enabling data integration, real-time monitoring, and decision support across clinical and administrative functions. Healthcare organizations are increasingly investing in native analytics modules embedded within electronic health record (EHR) systems and standalone enterprise solutions capable of processing multimodal data. Epic Systems and Cerner, for instance, have integrated advanced analytics engines into their core platforms, allowing health systems to conduct risk stratification, readmission forecasting, and quality benchmarking without external tools. Furthermore, the rise of vendor-neutral archives (VNAs) and AI-powered diagnostic software has expanded the scope of analytics applications. The U.S. Food and Drug Administration has cleared more than 200 AI-based diagnostic software tools since 2020, many of which rely on proprietary algorithms for image interpretation and predictive modeling. These tools are not only improving diagnostic precision but also reducing clinician workload. With healthcare data volumes doubling every 18 months, as estimated by Johns Hopkins Medicine, scalable software solutions are becoming indispensable for managing complexity. The shift toward value-based care further amplifies demand, as providers require continuous performance tracking and compliance reporting functions inherently dependent on robust software infrastructure.

The services segment is emerging as the fastest-growing component of the healthcare analytics market and is projected to expand at a CAGR of 18.7% from 2025 to 2033. This surge is driven by the increasing need for implementation, integration, training, and managed analytics services, particularly as healthcare institutions adopt complex AI and machine learning platforms. Unlike off-the-shelf software, advanced analytics systems require extensive customization to align with institutional workflows, data architectures, and regulatory requirements. A large share of hospitals engaged third-party consultants for analytics deployment, citing a lack of internal expertise as the primary reason. Moreover, post-implementation support is critical a significant portion of analytics initiatives fail within two years without ongoing optimization and change management. Managed analytics services, where vendors operate and maintain systems on behalf of providers, are gaining traction, especially among mid-sized hospitals. For example, outsourced its predictive analytics operations to a specialized firm, achieving an improvement in sepsis detection. Additionally, regulatory compliance services are in high demand due to evolving data privacy laws; healthcare organizations now allocate a notable share of their analytics budgets to consulting and compliance support. As analytics ecosystems grow more intricate, the reliance on expert services is becoming a strategic necessity rather than an auxiliary function.

By Application Insights

The clinical analytics segment stood as the largest application in the healthcare analytics market by capturing an estimated 36.3% of the total share in 2024. Its dominance is due to the urgent need to enhance diagnostic accuracy, reduce medical errors, and improve patient outcomes through data-driven clinical decision-making. With diagnostic errors contributing to a portion of patient deaths in the U.S., as highlighted in a study published in BMJ Quality & Safety, healthcare providers are turning to clinical analytics to mitigate risks. Predictive models analyzing EHRs, lab results, and imaging data have demonstrated a reduction in adverse drug events. In radiology, AI-powered analytics tools have improved lung nodule detection rates. The integration of clinical decision support systems (CDSS) into EHRs has become standard practice. These systems alert clinicians to potential drug interactions, sepsis onset, and deteriorating vital signs in real time. Furthermore, the rise of precision medicine has intensified demand for genomic and phenotypic data analysis. As clinical workflows become increasingly dependent on real-time data interpretation, clinical analytics has evolved from a supportive tool to a core operational function, cementing its leadership in the application landscape.

Population health analytics is the fastest-growing application segment and is anticipated to grow at a CAGR of 19.3% between 2025 and 2033. This acceleration is fueled by the global shift from fee-for-service to value-based care models, where providers are financially accountable for patient outcomes across entire populations. Under programs like the Medicare Shared Savings Program, several accountable care organizations (ACOs) in the U.S. are using analytics to monitor chronic disease prevalence, vaccination rates, and hospitalization trends among enrolled populations, as documented by the Centers for Medicare & Medicaid Services. The World Health Organization emphasizes that effective population health management can reduce preventable hospitalizations, a critical goal for overstretched health systems. Analytics platforms now integrate social determinants of health (SDOH) data such as housing stability, food insecurity, and transportation access into risk models. Additionally, public health agencies are leveraging analytics for disease surveillance. With aging populations and rising multimorbidity, the ability to proactively manage health at scale is making population health analytics indispensable.

By End User Insights

The healthcare providers segment was the leading end-user in the healthcare analytics market by holding 56.4% of share in 2024. This preeminence is driven by the dual pressures of improving clinical outcomes and achieving operational efficiency in an era of rising patient volumes and staffing shortages. Hospitals and clinics are deploying analytics to optimize bed utilization, reduce length of stay, and predict patient no-shows. Besides, analytics supports clinical quality improvement providers using real-time dashboards for sepsis detection have reduced mortality rates. The widespread adoption of electronic health records has enabled longitudinal patient tracking, essential for care coordination. Moreover, provider consolidation into integrated delivery networks (IDNs) has amplified the need for centralized analytics platforms. So, analytics is increasingly viewed as a force multiplier, enabling fewer clinicians to manage larger patient panels effectively. These operational and clinical imperatives solidify providers’ position as the dominant end-user segment.

Pharmaceutical and biotechnology companies represent the fastest-growing end-user segment, projected to expand at a CAGR of 20.1% from 2025 to 2033. This growth is propelled by the integration of real-world data (RWD) and real-world evidence (RWE) into drug development, regulatory submissions, and post-market surveillance. The U.S. FDA now accepts RWE for label expansions. Analytics enables pharma firms to analyze EHRs, claims data, and patient registries to identify eligible trial participants, reducing recruitment time. Roche’s use of AI-driven analytics in oncology trials shortened patient enrollment, accelerating time-to-market. Additionally, pharmacovigilance has been transformed Pfizer employs natural language processing to scan millions of social media posts and medical forums, detecting adverse events faster than traditional methods. The rise of personalized medicine further intensifies demand. So, analytics offers a strategic lever to enhance efficiency, reduce failure rates, and ensure regulatory compliance, driving rapid adoption across the sector.

By Delivery Mode Ingsights

The on-premise deployment remained the prominent delivery mode in the healthcare analytics market by representing 54.4% of share in 2024. This dominance is largely attributable to the stringent data security and regulatory compliance requirements inherent in healthcare, particularly in regions with strict privacy laws such as HIPAA in the U.S. and GDPR in Europe. Large health systems, especially academic medical centers and government hospitals, prefer on-premise solutions to maintain full control over sensitive patient data. Additionally, on-premise deployments offer higher customization and performance for compute-intensive tasks such as genomic analysis and AI model training. The U.S. Department of Veterans Affairs continues to rely on on-premise systems for its nationwide analytics network, citing security and interoperability with VistA EHR as key factors. Despite the rise of cloud alternatives, concerns over data breaches reinforce institutional preference for localized data control.

The cloud-based deployment is the fastest-growing delivery mode, expected to grow at a CAGR of 19.8% in the coming years. This rapid ascent is driven by the scalability, cost-efficiency, and rapid deployment capabilities offered by cloud platforms, particularly for mid-sized hospitals and emerging markets. Cloud solutions eliminate the need for large capital expenditures on servers and IT staff, making advanced analytics accessible to resource-constrained organizations. Many healthcare providers are either fully or partially migrated to cloud-based analytics, citing faster implementation and automatic updates as key advantages. Amazon Web Services and Microsoft Azure now host analytics platforms for a notable portion of U.S. health systems, enabling real-time data sharing across geographically dispersed facilities. The UK’s National Health Service has adopted a cloud-first policy, reducing data processing time for cancer diagnostics. Additionally, cloud environments facilitate collaboration in research. The integration of AI and machine learning toolkits within cloud platforms further accelerates adoption, positioning cloud-based delivery as the future backbone of agile, scalable healthcare analytics.

REGIONAL ANALYSIS

North America Healthcare Analytics Market Insights

North America led the global healthcare analytics market by commanding a 42.4% market share in 2024. The region’s dominance is anchored in its advanced digital health infrastructure, strong regulatory push for data-driven care, and high healthcare expenditure. The United States, in particular, has been a pioneer in adopting analytics for value-based care, with the Centers for Medicare & Medicaid Services mandating quality reporting through programs like MIPS and ACOs. Private investment is robust. Canada complements this ecosystem with national digital health strategies and interoperability frameworks. The presence of leading tech firms and research institutions ensures continuous innovation, solidifying North America’s position as the epicenter of healthcare analytics advancement.

Europe Healthcare Analytics Market Insights

Europe holds a significant market share, which is driven by strong public health systems and coordinated digital transformation initiatives. The European Union’s Digital Single Market strategy has prioritized cross-border health data exchange. Germany leads in analytics adoption, with many university hospitals using predictive models for ICU management, as reported by the German Medical Association. The UK’s National Health Service has integrated AI into radiology and pathology, reducing diagnostic delays. Additionally, the EU’s Horizon Europe program has allocated substantial funds for health data research, fostering innovation. Despite these challenges, the commitment to interoperability and equity-driven care ensures Europe remains a major force in the global analytics landscape.

Asia-Pacific is poised for rapid expansion due to digital health modernization across key economies. China has launched its “Healthy China 2030” initiative, investing billions of dollars in digital infrastructure, including AI-powered diagnostics and regional health data centers. Japan, facing a super-aged society, employs analytics in elderly care. While challenges like data silos and workforce shortages persist, government-backed digital transformation is accelerating analytics adoption, positioning Asia-Pacific as a high-growth frontier.

Latin America is witnessing steady growth driven by public health modernization and private sector investment. Brazil leads the region with its e-SUS program. Colombia has implemented a national telehealth network, integrating analytics for maternal and child health monitoring in remote areas. However, infrastructure disparities remain. With increasing smartphone penetration and government support, Latin America is gradually building the digital foundation necessary for scalable analytics deployment.

The Middle East and Africa collectively represent a notable share of the global market, with significant variation across subregions. Gulf Cooperation Council (GCC) countries are spearheading adoption. The UAE has launched the Dubai Health Strategy 2026, integrating AI into public health surveillance. In contrast, Sub-Saharan Africa faces systemic challenges. However, mobile health innovations are bridging gaps. South Africa’s National Health Insurance program relies on analytics for fraud detection in claims processing. While infrastructure and funding constraints persist, strategic investments in digital transformation are laying the groundwork for future analytics expansion across the region.

KEY MARKET PLAYERS

A list of notable companies playing a promising role in the Global Healthcare Analytics Market is SAS Institute Inc., McKesson, Optum Inc., IBM Corporation, Truven Health Analytics Inc., Cerner Corporation, Verisk Analytics Inc., Allscripts Health Solutions, Oracle Corporation, MedeAnalytics, Inovalon Inc., and Health Catalyst.

TOP LEADING PLAYERS IN THE MARKET

IBM Corporation

IBM Corporation has been a pioneering force in healthcare analytics through its Watson Health platform, which leverages artificial intelligence to derive clinical and operational insights from complex health data. The company has focused on integrating cognitive computing into oncology, drug discovery, and population health management, enabling providers to personalize treatment pathways and improve decision-making. IBM’s long-standing collaborations with academic medical centers and life sciences organizations have positioned it as a trusted innovator in data-driven healthcare. Its emphasis on ethical AI and explainability has influenced industry standards, while its cloud-based analytics tools support scalable deployment across diverse healthcare environments. By bridging advanced computing with clinical workflows, IBM continues to shape the evolution of intelligent health systems globally.

Optum

Optum, Inc., a subsidiary of UnitedHealth Group, plays a central role in advancing healthcare analytics through its end-to-end data and technology solutions for payers, providers, and pharmaceutical clients. The company excels in aggregating real-world data from insurance claims, EHRs, and patient interactions to generate actionable insights for cost management, care coordination, and risk prediction. Optum’s analytics platforms are deeply embedded in value-based care models, supporting accountable care organizations and government programs with performance tracking and intervention planning. Its integrated approach combining data assets, clinical expertise, and predictive modeling enables comprehensive health system optimization. With a vast network of provider partnerships and a strong focus on population health, Optum has become a dominant force in transforming data into strategic healthcare intelligence.

Cerner Corporation

Cerner Corporation, now part of Oracle Health, has been instrumental in embedding analytics directly into electronic health record systems used by hospitals and health networks worldwide. The company’s platforms enable real-time clinical decision support, operational dashboards, and quality reporting, allowing providers to monitor patient outcomes and regulatory compliance seamlessly. Cerner’s strength lies in its ability to unify disparate data sources across care settings, facilitating interoperability and longitudinal patient tracking. Its early adoption of health information exchange frameworks has supported large-scale public health initiatives and pandemic response efforts. By designing analytics as an intrinsic component of clinical workflows rather than a standalone tool, Cerner has redefined how healthcare organizations leverage data for both immediate care delivery and long-term strategic planning.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

One major strategy employed by leading players is the deep integration of artificial intelligence and machine learning into core analytics platforms to enhance predictive accuracy and automate clinical and operational insights. Companies are prioritizing the development of intelligent algorithms that can interpret unstructured data, such as physician notes and imaging reports, to deliver context-aware recommendations. This shift enables proactive care interventions and reduces clinician burden, making analytics more clinically relevant and actionable.

Another key approach is strategic collaboration with healthcare providers, payers, and research institutions to co-develop tailored analytics solutions that align with real-world clinical workflows and regulatory requirements. These partnerships facilitate access to diverse, high-quality datasets and ensure that tools are validated in live environments, increasing adoption and trust among end users.

A third prevalent strategy is the expansion of cloud-based delivery models to improve scalability, interoperability, and remote accessibility of analytics tools. By migrating platforms to secure cloud infrastructures, companies enhance data sharing across decentralized systems, support real-time analytics, and reduce the IT burden on healthcare organizations, particularly smaller providers lacking in-house technical resources.

RECENT HAPPENINGS IN THE MARKET

The competitive landscape of the healthcare analytics market is characterized by a dynamic interplay of technological innovation, strategic positioning, and domain-specific expertise. Established health IT vendors, tech conglomerates, and specialized analytics firms are vying for dominance by differentiating their offerings through advanced AI capabilities, seamless integration with clinical systems, and robust data governance frameworks. The market is witnessing a shift from generic analytics tools to highly specialized solutions tailored for clinical decision support, revenue cycle optimization, and population health management. Differentiation increasingly hinges on the ability to deliver not just data insights, but clinically interpretable, actionable intelligence that aligns with provider workflows. Companies are investing heavily in user experience design, algorithm transparency, and regulatory compliance to build trust among healthcare professionals. Mergers and acquisitions are common as firms seek to consolidate data assets, expand geographic reach, and enhance technical capabilities. The convergence of EHRs, wearable data, and real-world evidence is creating new battlegrounds for innovation, particularly in predictive modeling and personalized medicine. As healthcare systems worldwide prioritize data-driven transformation, the competition is intensifying around agility, interoperability, and the capacity to deliver measurable improvements in patient outcomes and operational efficiency.

RECENT MARKET DEVELOPMENTS

- In February 2024, Oracle completed the full integration of Cerner’s analytics platforms into its cloud infrastructure, enabling enhanced data interoperability and AI-driven decision support for healthcare providers using Oracle Health solutions.

- In June 2023, IBM launched a new federated learning framework within Watson Health, allowing hospitals to collaboratively train AI models on decentralized data without compromising patient privacy or data sovereignty.

- In September 2023, Optum expanded its real-world data network by forming a strategic alliance with a national primary care consortium, enhancing its ability to generate insights for chronic disease management and value-based care programs.

- In January 2024, Microsoft partnered with a leading European hospital group to deploy its cloud-based healthcare analytics suite, focusing on predictive modeling for ICU admissions and resource allocation.

- In March 2024, Google Health introduced a new natural language processing engine for clinical documentation, enabling automated extraction of insights from unstructured physician notes across integrated delivery networks.

MARKET SEGMENTATION

This research report on the global healthcare analytics market has been segmented and sub-segmented based on type, application, end-user, and region.

By Component

By Application

- Clinical Analytics

- Financial Analytics

- Operational Analytics

- Population Health Analytics

- Other Applications

By Deployment Mode

By End User

- Healthcare Providers

- Healthcare Payers

- Pharmaceutical & Biotechnology Companies

- Other End Users

By Delivery Mode

- On-Premise Deployment

- Cloud-Based Deployment

- Web-Based Deployment

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

link

![Average Cost of Medical School [2025]: Yearly + Total Costs](https://educationdata.org/wp-content/uploads/2025/09/page-1.png "Average Cost of Medical School [2025]: Yearly + Total Costs")